Apple Analysis $AAPL

An Overview Of The World’s Most Valuable Company

Key Metrics AAPL 0.00%↑

Market Cap = $2,140B

EV = $2,210B

FCF = $111.44B

FCF Yield = 5.2%

ROIC = 50.2%

EBIT = $122B

EV/EBIT = 18.15

5 Year Rev CAGR =8%

10 Year Rev CAGR =9%

Intro

Apple is the world’s largest company by market cap. It’s currently the only business in the world with a valuation of over $2 trillion.

Steve Jobs, touted as one of this generation's greats, is famously recognised as the innovator behind Apple. He founded the company with Steve Wozniak in 1976, out of his garage.

The launch of the Apple I was followed by the Apple II in 1977. The Apple II revolutionised the computer industry with the introduction of the first-ever colour graphics. Sales grew exponentially, from $7.8 million in 1978 to $117 million in 1980, the same year Apple went public.

Wozniak left in 1983 and Jobs followed in 1985, going on to found NeXT Software and purchase Pixar.

As Microsoft squeezed Apple out of the market over the following decade, the board opted to purchase NeXT and reinstate Jobs as the CEO.

Jobs revamped the computers and introduced the iBook, iPod and eventually the iPhone in 2007.

Since Jobs' 1997 return, revenue has grown from $7 billion to over $394 billion in 2022, a CAGR of 17.5%. Jobs passed away in 2011, but Apple continues his legacy with Tim Cook at the helm as CEO.

The Apple Ecosystem

Often referred to as a walled garden, the Apple Ecosystem creates an enhanced user experience through increased interaction between devices.

The Ecosystem encourages users to ‘level up’ and purchase further hardware. It creates system-wide integration and allows Apple to design around several devices.

The backbone of the entire Apple Ecosystem is Apple ID. Apple ID is used to register each device to the users account.

Some examples include using an Apple Watch to unlock a Mac, playing music on an iPhone before transferring it to the HomePod and receiving iMessages on all Apple devices.

Apple’s Ecosystem creates an experience that is greater than the sum of its parts. This improves the customer journey and locks the user into the system.

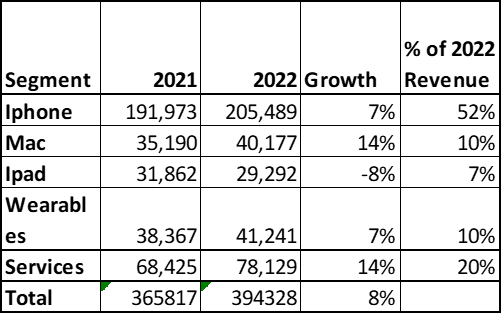

Business Segments

Apple’s segments the business revenue into 5 key areas;

iPhone

Mac

iPad

Wearables, Home and Accessory

Services

iPhone - 52% of Revenue

")

First launched in 2007, the iPhone has been the driving force behind Apple’s turnaround and global conquest.

Generating 52% of 2022’s revenue, the company annually releases iPhone models and iOS software updates. The most recent model was 2022’s iPhone 14 and iOS 16. There are more than 1.2 billion active iPhones worldwide as of 2022. The iPhone accounts for a reported 15.6% of the global smartphone market.

Despite being on the market since 2007, iPhone revenue still grew 10% year-over-year to a September quarter record of $42.6 billion. Growth is being driven in emerging markets. Thailand, Vietnam and Indonesia doubled sales in 2021 and India achieved a record year.

According to Four Week MBA, the iPhone generates a gross margin of approximately 45%. Apple is one of the few hardware companies that can command such a significant margin, with competitors typically employing a razor blade model (low initial profit, higher on add-ons).

Apple locks customers into recurring handset purchases by saving personal data to iCloud. This ensures thousands of photographs, apps, messages and files can be instantly transferred to a newer model. This makes a handset upgrade almost instantaneous, keeping customers in the ecosystem.

Apple has infamously been accused of reducing the processing power and battery life with repeated software updates, forcing customers to upgrade regularly. Apple claims it would never purposely shorten the lift of older products, but is still facing multi-million pound lawsuits.

Mac - 10% of Revenue

The descendant of the 1984 Macintosh, the Mac is now responsible for $40 billion of global revenue.

First unveiled in the acclaimed advert, directed by Ridley Scott, the Macintosh was named after a type of apple. The success of the first model was largely down to the ease of use and reasonable purchase price.

The Mac has evolved considerably since 1984, the launch of 2022’s upgraded MacBook Air and MacBook Pro saw sales increase 25% year-over-year, which drove the install base to an all time high.

Both models are powered by the new M2 chip. The introduction of the M1 chip in 2020 was the first step toward transitioning away from the Intel chips which the company has used since 2006. The M1 & M2 chips were designed by Apple and manufactured by TSMC. The M2 chip employs TSMC’s 5nm technology, with an M2 Pro expected to follow with 3nm. The introduction of the M Series chips will be a key component in creating the next generation of products and complete a vertical integration.

iPad - 7% of Revenue

First launched in 2010, the iPad was originally intended to be released prior to the iPhone.

The iPad now consists of several versions to meet price and demand. These include the Pro, Air and Mini.

Prices vary from £369 to £1,249, depending on the model. The iPad acts as a practical medium between MacBook and iPhone.

Since 2010, Apple has released over 30 iPad models. The 10th-generation iPad was announced on October 18, 2022.

In the fourth quarter of 2022, iPads generated $7.2 billion in revenue, down 13% from the same quarter last year. A direct comparison is difficult, as Apple introduced new iPads during the fourth quarter of 2021.

With only 7% of revenue generation, the iPad is no cornerstone of the Apple business model, however it remains key to introducing old and new users to the Apple ecosystem, in particular the App Store. Generation Alpha, those born after 2010, are often referred to as iPad kids.

Wearables, Home and Accessories - 10% of Revenue

The $41 billion of revenue generated by the Wearables segment is impressive considering it did not exist a decade ago. This is a perfect example of Apple’s playbook of creating new markets with relatively low investment. The segment will generate over $200 billion in cumulative revenue in less than a decade!

Wearables include the Apple Watch and AirPods. AirPods dominate the Bluetooth headphone market, bringing in a reported $12 billion per year. This is nearly as much as Adobe and Uber’s overall revenue.

The Wearable segment is growing 10% year-over-year, driven by multiple new releases including; AirPods Pro, Apple Watch Ultra and the Apple Watch Series 8.

Starting with the 2020 iPhone 12 release, headphones were no longer gratuitously provided. This is another example of Apple encouraging users to ‘level up’ by upgrading to AirPods whilst reducing internal costs.

Services - 20% of Revenue

")

The company's services segment is led by the App Store and Apple Music but includes; iCloud, Apple Music, Apple TV, Apple Arcade, Apple News, Apple Fitness.

The services sector is high margin, low investment, and charges users and developers a fee to engage.

The Services segment achieves a gross margin of 70.5%, in comparison to Products gross margin of 34.6% and 42.3% for the company overall.

Apple highlighted they have over more than 900 million paid subscriptions in September’s earnings call. Services revenue achieved a record $78 billion in 2022, up 14% on the previous fiscal year.

The App Store

Apple only allows iOS users to download and access apps via the App Store.

The App Store has often been touted as a toll road to the internet. Apple has been criticised for their aggressive 30% commission on apps and in-app purchases. In 2021, Apple introduced the ‘Small Business Programme’, which reduced commission to 15% for developers earning under $1m per year.

The App Store offers developers 5 business models;

Free

Freemium - users pay nothing to download the app but can purchase optional premium features

In app purchases

Paid - users pay to purchase the app

Paymium - Users pay for the and can also make in app purchases

The Apple App Store has 2 million apps available for download.

In 2021, Apple reported that it paid developers a record $60 billion. This implies the App store generated annual revenue of approximately $25 billion.

Licensing

Apple receives licensing payments from various third parties. Around $15 billion of this revenue is estimated to come from Google, who pay an annual fee to remain the default search engine across Apple devices.

Apple Care

Care is essentially an insurance for customers, providing an extended warranty and technical support for devices. Customers pay an upfront cost to extend their warranty, whilst making a further payment against any further damage.

Care starts at around $149 for an iPhone, up to $399 for a 16-inch MacBook Pro.

It’s estimated that Care generates around $10 billion annually.

Apple Music

The streaming service has the world's largest music catalogue with over 100 million songs. Apple Music has approximately 80 million paying customers, second only to Spotify, who boast 160 million subscribers.

Subscriptions start at £4.99 / $10.99, which implies Apple generates over $7 billion annually from Music.

Apple Pay

First introduced in 2014, Apple Pay allows users to save their credit and debit cards to their phone’s wallet, making the plastic version redundant.

Income from payments comes from the 0.15% fee that is charged to the issuer of the card. This equates to a £0.15 from a £100 purchase.

Apple Pay has been one of the major winners as Covid accelerated the shift to a cashless society. Reported to have over 500m users in January, Tim Cook described the growth of Apple Pay as ‘stunning’. Based on Cook’s terminology, Pay appears to be on an upward trajectory.

Apple is in the process of introducing Apple Pay Later with the aim of breaking into the buy-now-pay-later sector. Pay is not only giving the company a share of the customers wallet, but reducing friction for future purchases from the Ecosystem (described earlier).

A Look at the Numbers

Apple has weathered the storm better than its FANGAM counterparts (down 26% YTD). Bolstered by recent successful product launches, customers spent more on hardware and software as they transitioned to working from home in 2020 & 21.

The narrative that ‘Apple is a market leading technology company with a walled garden’ remains intact, but is Apple as safe an investment as first appears? The full effects of the macro crisis and return to work have not yet affected revenue, but could still play out.

Buffet famously bought Apple in 2016, when the PE was less than half of 2022’s average.

Revenue and income have grown steadily, achieving a CAGR over the past 5 years of 8%. This is reliable single figure growth, but does it justify Apple’s PE of 22?

Gross profit margins have increased as the Services segment shouldered a larger portion of the revenue.

Apple has responded to their noteworthy cash pile by repurchasing 4% of shares outstanding per year, paying out 15-25% of income as dividends. That’s a reduction of 35% of shares outstanding since 2012!

This has added significant, unseen value, for shareholders.

Management have maintained a constant level of debt, but will likely step carefully with issuance of future debt as interest rates continue to rise.

Capex has reduced over the past 5 years, whilst R&D has hovered at around 6% of revenue. This raises the question, are Apple under investing? Capex has been lower than depreciation for several years.

Apple is a truly exceptional company, it can create growth with minimum investment. However, the company competes in the fast moving hardware and software sector. Meta’s ($META) Capex/Revenue ratio could be as high as 20% in 2023. Is the lack of investment sustainable?

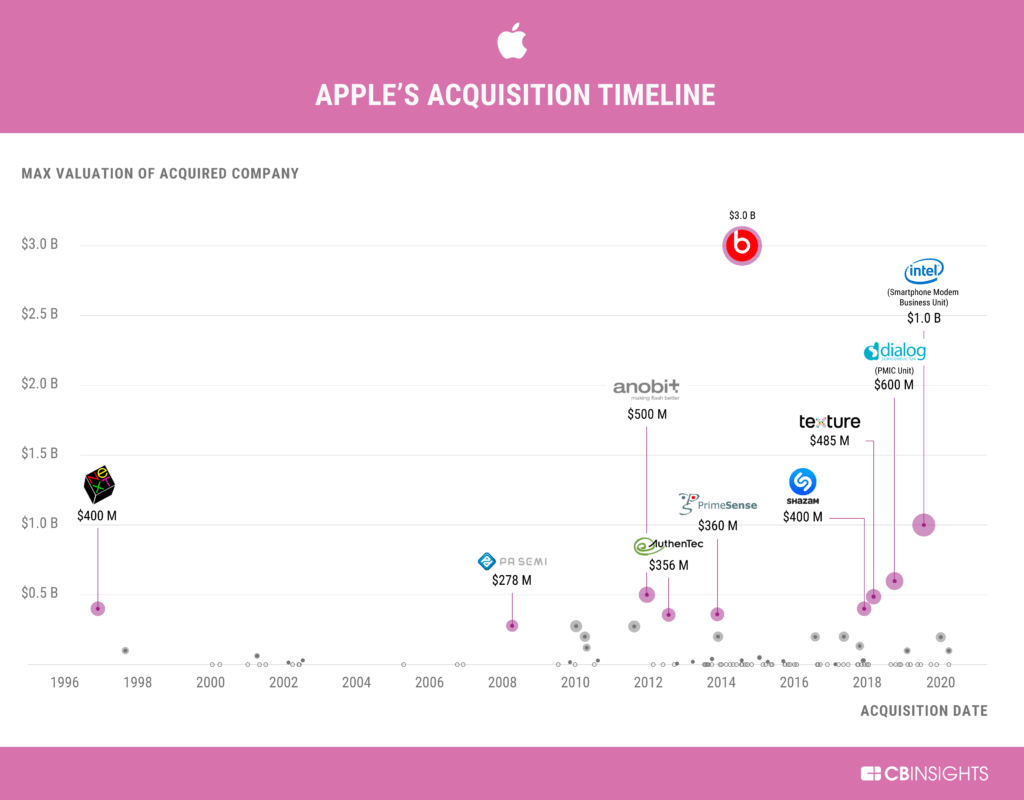

Acquisitions

Another key use of Apple’s cash piles could be strategic acquisitions. In 2019, Tim Cook told CNBC that “Apple buys a company every few weeks”. Apple historically has purchased companies with the view of incorporating their technology into their own products. For example, Israeli company PrimeSense was the innovation behind Apple’s FaceID.

Apple’s largest acquisition to date was the $3 billion purchase of Beats. Compare that to Microsoft’s largest, Activision for $67 billion.

Microsoft appears to be strategically acquiring to set themselves up for the next generation of computing, whilst Apple are purchasing technology to incorporate into next year's hardware.

Tim Cook has done an incredible job of maintaining steady growth, whilst returning value to shareholders through buybacks. This raises the question, how long can Apple’s low investment rate be maintained when compared to competitors?

Bull Points

The Brand/Ecosystem

Apple’s brand is the world’s most valuable, according to Interbrand.

You can’t explain the brand, it’s taken decades to reach this point. It’s a mix of art and technology. The white AirPods are instantly recognisable. Customers queue overnight to buy the latest product. The hardware has achieved a cult-like status that customers build their persona around.

This creates loyal users who find it difficult to give up Apple products (myself included).

The white headphones, and now AirPods, have made Apple products recognisable for over two decades

Emerging Market Opportunity

Apple's recent growth has come from several large emerging markets. In the most recent quarter the company achieved double-digit growth in India, Southeast Asia and Latin America.

Growth could stagnate in the West, but it’s clear there’s major demand in developing economies.

Advertising Opportunity

In the most recent earnings call, Tim Cook reported that advertising revenue was “clearly not large”, although Insider Intelligence, a market research firm, estimates that Apple brings in $4 billion a year from ads.

Apple’s recent privacy change cost Facebook a reported $10-12 billion in revenue, whilst Google only remains in the fold due to their annual multi-billion dollar stipend. Apple’s closed system ensures they can slam the door on both companies whenever they see fit.

As of September 2022, Apple had around 250 employees working on its ad platforms, according to an analysis of LinkedIn data by the Financial Times. Investment bank Evercore ISI estimates Apple will have a $30 billion ad business by 2026.

VR / AR

The introduction and in-house design of the M chip series could be a vital building block in the development of AR & VR technology. Apple is reported to be developing at least two AR projects that include an augmented reality headset, which will be released in 2023, followed by augmented reality glasses.

Customers are comfortable wearing Apple hardware, the proof is the hundreds of millions of AirPods in ears and Watches on wrists. A transition to Augmented Reality hardware feels natural and could blow Zuckerberg’s Quest 2 out of the Metaverse.

Untapped Revenue From the Closed Ecosystem

Regular podcast listeners will be more than familiar with adverts or hosts who encourage users to upgrade. With Apple Pay on every iPhone, it appears to be a no-brainer to allow listeners to double tap to purchase a freemium model, whilst Apple takes a healthy commission.

This is just a single example of how Apple can generate increased revenue with little upfront costs.

Remember, the total $185 billion of cumulative Wearables revenue did not exist a decade ago. As the ecosystem continues to grow, we’ll undoubtedly see the introduction of a number of billion dollar revenue generators, unpredictable to outsiders, but obvious in hindsight.

Bear Points

Over Reliance on iPhone

The iPhone was the catalyst for Apple’s transformation, but could be their Achilie’s Heel.

Generating 52% of revenue and acting as the lynchpin for the ecosystem, the iPhone is Apple's driving force. However, Apple’s market share has dropped 6% in the past year. This may be a result of the cost of living crisis or Apple’s competitors releasing cheaper phones. Google recently introduced the Google Pixel Pro 7, with prices starting at £599, £250 cheaper than the iPhone 14.

The iPhone was launched during the financial crisis, but has never had to experience extreme macro challenges. An overpriced or underwhelming hardware in future models could lead to the entire ecosystem coming unstuck.

Failing To Innovate

A recurring criticism of Apple since Jobs’ death has been their lack of innovation. Tim Cook has followed the playbook wonderfully, building on Jobs' initial framework. It’s unfair to completely criticise lack of innovation. AirPods, first released in 2016, are rumoured to have sold over 100 million units. And the introduction of the M1/M1 chip could be a game changer, but on the surface, Apple hasn't released anything truly revolutionary since the iPhone.

Microsoft and Amazon have invested in Azure and AWS respectively. Cloud growth has been an explosive sector and seems to be an obvious miss from Cook and Co.

Facebook is investing heavily in the metaverse plus their AR / VR bets. Apple will be late to the party if they release their AR headset in 2023.

There’s no doubt the company will be assessing how funds are deployed. As competitors diversify and double down on acquisitions, how long can Apple’s playbook continue to deliver?

Exposure to China and TSMC

Apple generated 22% of revenue from China in 2022 vs 17% in 2018. This is undoubtedly a key marketplace for the company. The ongoing narrative of tensions between China and the US show no signs of ending. If China was to ban Apple products, it would be a devastating blow.

Most big tech companies would be in trouble if China were to annex Taiwan. All current chips are manufactured primarily in Taiwan by TSCM. TSMC is building two fabs in Arizona as Apple seeks to move manufacturing to the United States and mitigate this risk.

Conclusion

Apple is the most valuable company to have ever existed. The diversified business model is held together by the success of the iPhone and the closed off ecosystem. Apple owns the stack, from software to the M1/M2 chip and hardware. The in-house chip designs will be key to the next stage of devices.

That doesn’t take away from the fact the company is reliant on the success of the iPhone. Single figure growth is only going to maintain a relatively lofty valuation for so long. Services revenue will shoulder more of the burden, but the company appears to be missing the wow factor of Azure or AWS.

In the midst of the greatest financial crisis of the decade, Apple shares are one of the last standing fortresses. Income shows no signs of slowing down, the 2022 fiscal year set annual records for iPhone, iPad and Mac, but the full affects of the cost of living increase could come into play in 2023.

If Jobs lay the foundations, Tim Cook has built the infrastructure. He has performed magic for shareholders since becoming CEO. A dollar invested when he took charge is now a 10 bagger - ignoring buybacks and dividends!

He’s delivered growth through minimal investment, whilst reducing shares outstanding by 35%. The question remains, can Apple continue to deliver from the same playbook if competitors outspend them?

It’s not obvious, to an outsider looking in, where Apple's next decade of growth will come from. What is obvious is that it’s going to require investment.

It would be unwise to bet against Apple, the ‘lack of innovation’ remarks were being made in 2016 - the same year Carl Ichan sold and Buffet bought. A decade ago, Wearables, Pay or Music hadn’t even launched. Shareholders will hope that Cook and Co can deliver the same magic well into the next decade.