Duolingo Deep Dive $DUOL

The bird is the word 🦉

DUOL 0.00%↑ Metrics (at time of publication)

Market Cap = $5.52B

Cash = $1.01B

Cash + Securities = $1.12B

EV = $4.51B

EV - Securities = $4.4B

FCF = $0.35B

EBIT = $0.11B

Summary Ratios

EV/EBIT = 40.9

EV (minus securities)/EBIT = 40

FCF Yield = 6.29%

Debt/Equity = n/a

Return on Equity = 36.25

Dividend Yield = n/a

5 Year Revenue CAGR = 35%

Simply Wall St DCF price - $476.69

Secret Sauce DCF - $228.5

1. Introduction

Duolingo is a product I have experience with - I once achieved a 300 day streak (not so humble brag below). This was during the pandemic. As normal life returned, my discipline, and streak, fell away.

Because of my engagement with the app, I have always kept an eye on the share price. The stock blew up in 2021, reaching around $200, before losing about 77% of its value!

The share price recovered as the fundamentals improved, hitting highs of $530 dollars in May 2025, but has since fallen by 77% to $116. At this point, it’s worth a deep dive.

The Duolingo App is the world’s most popular way to learn languages. The app offers a freemium service, with courses in over 40 languages. With over 100 million monthly active users, it is the top-grossing app globally in the Education category on both Google Play and the Apple App Store. Math, Chess and Music courses are the most recent additions and can all be accessed through the app.

Our mission is to develop the best education in the world and make it universally available. - Duolingo Company Mission

Duolingo appears to have solved one of the hardest problems in education by getting users to regularly engage by leveraging the gamified streak mechanism. Users return to maintain their streaks.

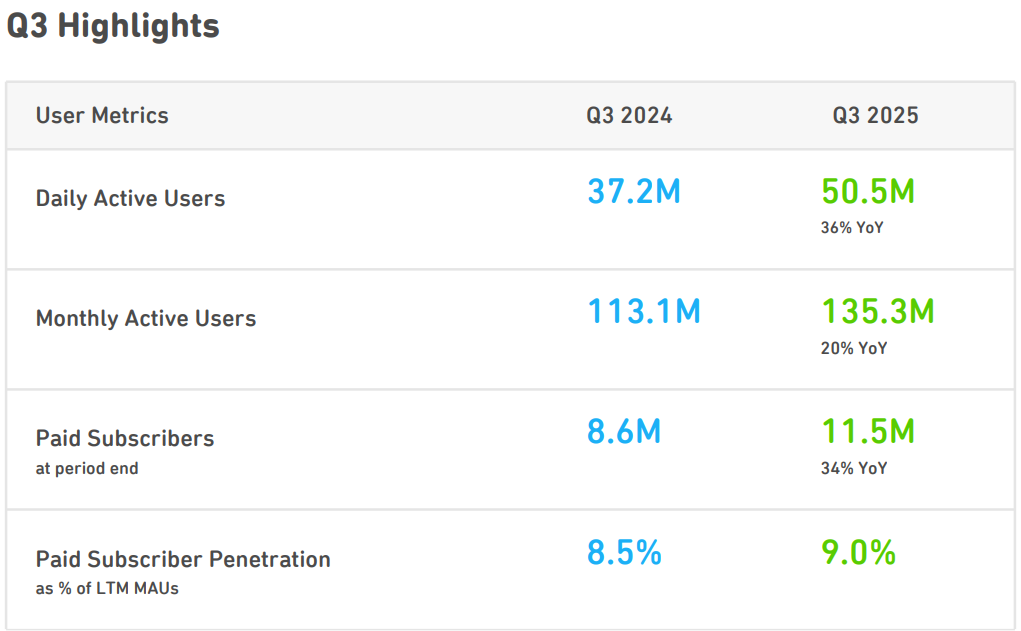

Since 2019 the platform has grown daily active users (DAU), by more than 10 times. In the most the recent quarter DAUs had increased by 36% YoY.

Duolingo has gamified learning, making it enjoyable rather than a chore. The business operates like a Silicon Valley product company that teaches languages, rather than an ed-tech. The company’s advantage is the relentless product improvement that has been honed with thousands of A/B experiments, with a ruthless focus on engagement.

2. The Product & Brand

Duolingo is the world’s leading mobile learning platform and the flagship app has become the most popular way to learn a language. It consistently ranks as the top-grossing education app on both the Google and Apple app stores. The company has largely achieved success through word-of-month and socially edgy marketing.

The app teaches over forty languages, though user engagement is not evenly distributed across the 40. The top languages; Spanish, English, French, German and Italian, make up the majority of demand. Users tend to engage with the app to ‘productively waste time’ rather than as a serious educational tool.

What keeps users coming back is is gamification and behavioural mechanics. Points, streaks, levels and leader boards ensure that users create a daily habit. The streak is now a point of pride amongst users, some of whom have practiced for thousands of days in a row. The ongoing improvements and and user retention methods have worked incredibly since IPO, with the DAU base having grown more than 10X since 2019.

Duolingo is fundamentally a product-led company. Approximately 16% of staff work on design and more than 380 of the 830+ employees are engineers. The organisation runs thousands of A/B tests each year across sign-up, retention, conversion and user flows. The volume of testing is closer to a Meta-scale consumer platform than ed-tech app.

The company tends to focus aggressively on engagement ratios rather than educational efficiency - with the long term view that users must be on the app in the first place before they can learn.

The product has expanded beyond language education and into math, music and chess. Chess launched within nine months after the initial concept and has reportedly surpassed math and music in users, with retention slightly higher than languages.

Management had suggested that that educational efficiency is improving annually, however, the financial gains linked to these improvements are differed. Improvements in learning support better retention, which expands the subscriber funnel and eventually increases earnings.

Duolingo’s brand is globally recognised. The mascot has become a cultural meme with the edgy content widely viewed across TikTok. This engagement across social media supports short term top-of-funnel growth.

The company’s roadmap focuses on three pillars; monetisation, user growth and teaching improvement. Monetisation changes are visible within a quarter, whilst user growth improvements take longer as subscribers lag DAUs, with educational improvements can take years to pull through.

The question remains - how far the product can expand beyond languages? Early evidence from math, music and chess is encouraging, but the ceiling depends on whether user engagement can permeate across categories and convert to monetisation. Is the TAM of these new products large enough to justify the diversification?

Competition in the education sector exists in the form of Coursera and Udemy on the skills/upskilling side, and Chegg in academic support. No direct competitor has matched Duolingo’s mobile engagement or consumer distribution.

3. Business Model

Duolingo operates a consumer freemium model that monetises only a small fraction of users. As DAUs grow, they convert to a small subset into paid subscribers. The paying users effectively subsidise the app and ongoing educational improvements

There is an lag between user growth and monetisation because casual users may take months or years before subscribing. Management remains confident that as the product becomes more engaging and more effective, subscription conversion will follow.

The underlying commercials are closer to a mobile game than traditional educational software. Most users engage casually, often for only a few minutes per day. This means that most users are less likely to upgrade a subscription, but instead focused on maintaining their streaks.

This creates a funnel where subscription penetration remains low relative to other consumer subscription businesses, but unit economics are extremely profitable for those who pay. Paid user growth remains strong, with both DAUs and revenue increasing more than 40% year-over-year while profitability continues to expand.

Users who can easily afford to subscribe often do not need the premium features, while those who would benefit most from subscription are less willing to pay, or be able to afford it. The long-term bet is that AI tutors, personalised feedback and higher-utility features will eventually justify premium tiers for serious learners, while the free layer continues to driver to acquire new users.

There are some insightful Reddit Threads that cover user debates on the benefit of subscribing.

Subscriptions (81% of Revenue)

The core paid product is Super Duolingo, which removes ads and unlocks premium features such as unlimited mistakes, exercise reviews, alongside speaking and listening modules. A family plan for up to six users makes it more cost effective for groups.

Pricing varies by market, with Super priced in the UK at £4.99/month or £59.99/year and in the US, $12.99/month or $84/year. While prices are presented monthly, billing is primarily annual, which front loads cash flow and improves working capital.

In 2023, Duolingo introduced Duolingo Max, a higher-tier offering. Max includes all Super features plus generative-AI-powered capabilities such as AI tutors, roleplay scenarios and personalised feedback. Max accounts for around 9% of subscribers and is built on OpenAI’s GPT-4 (and successor models), which Duolingo also uses to accelerate course creation.

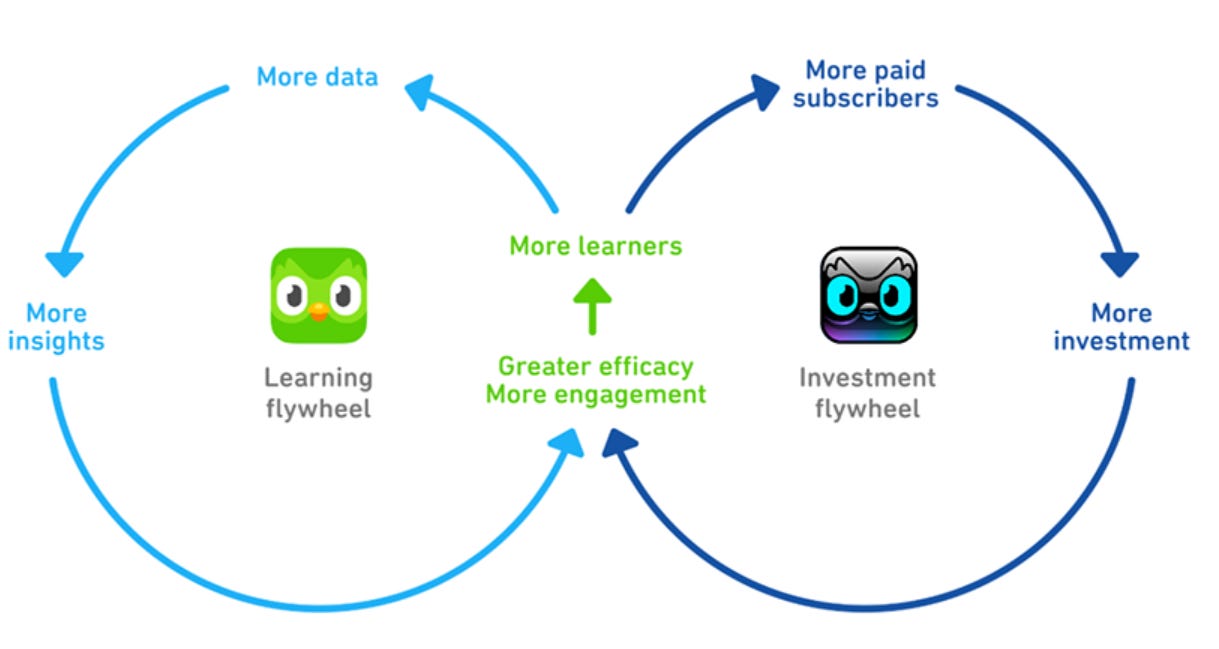

The long term focus ties directly into the company-wide flywheel. In this scenario the strategy is to scale AI tutors globally, while reducing costs to near-zero. The improved user experience should DAUs and in-turn subscribers, while resulting in a more efficient learning experience.

Advertising (7.3% of Revenue)

Advertising monetises free users who may never convert. Ads are shown between lessons and during breaks. The revenue offsets the cost to serve a large free user base without cannibalising subscription income.

Duolingo English Test (6.1% of Revenue)

The Duolingo English Test (DET) has evolved into a stand-alone business with international recognition. The test is now accepted by over 6,000 institutions worldwide, including all Ivy League universities and 99 of the top 100 US universities. It comprises of a 45–60 minute online session with identity verification and AI invigilation, with institutions able to benchmark scores against TOEFL and IELTS.

Unlike the core app, DET monetises directly and does not rely on a freemium funnel.

4. Customers & User Behaviour

Duolingo has reached a global user base with 50.5M daily active users, 135.3M monthly active users and 11.5M paying subscribers.

User growth has compounded at around 55% annually over the past three years, while bookings have grown approximately 45% per year over the same period. Growth remains global, with Asia now the fastest-growing region both in users and monetisation potential.

The user base diverges into two distinct cohorts. The first are hobbyists - casual learners who treat Duolingo as a productive alternative to scrolling on Instagram. These users drive DAU scale but are less inclined to pay for premium features.

The second cohort are serious learners, primarily non-native English speakers learning English for educational or economic mobility. Although this cohort is smaller in absolute numbers, they represent a materially higher ARPU opportunity, with willingness to pay for language acquisition in markets such as Asia and Latin America. More than 80% of the world’s language learners are learning English, and English learners account for around 46% of Duolingo’s DAUs. Before joining Duolingo, ~80% of users were not actively studying a second language, which highlights the product’s ability to create new learners rather than simply capture existing ones.

Retention and churn dynamics have improved meaningfully as gamification deepened. Churn declined from approximately 47% in 2020 to 37% by early 2023, with Western markets reaching 28% in late 2023. This places Duolingo among the strongest retention profiles in consumer education, though recent AI-driven product changes in 2025 triggered short-term user frustration and a dip in MAUs, demonstrating that retention requires continuous optimisation.

5. Geography & Revenue Mix

United States - 41.6% of revenue

United Kingdom - Previously 10% of revenue (company stopped reporting after 2022)

Rest of World (including UK) - 58.4%

Duolingo has already captured a significant portion of the US market and continues to expand internationally. The US accounts for 41.6% of revenue; the UK previously contributed around 10% before the company stopped reporting breakdowns in 2022. Collectively, the Rest of World now represents 58.4% of revenue, and more than half of bookings come from outside the US. International pricing sensitivity varies by platform type. iPhone users tend to offer higher-income and convert at higher rates, especially in emerging markets where mobile devices are the primary computing platforms.

Serious learners represent future opportunities but are disproportionately located in middle to low income countries. This has lead to a structural monetisation challenge, the segment most willing to pay more often resides in markets with lower purchasing power. Duolingo’s approach has been to expand premium tiers (Super and Max), experimenting with local pricing and relying on habit formation to convert over the longer term.

Competition varies by user segment. Serious learners face alternatives such as TOEFL and IELTS for accreditations, but upskilling and academic support competes with platforms like Coursera, Udemy and Chegg.

However, none of these competitors operate at the same scale or rely on DAU-driven behavioural loops. Duolingo’s true competition for casual learners is not ed-tech but attention devouring app including Instagram, TikTok, YouTube and mobile games.

Duolingo’s long-term opportunity does not depend on stealing market share from language schools or existing incumbents, but on activating non-learners and converting hobbyists into paying, long term subscribers.

6. Financials

Income Statement

Revenue has compounded at 36% annually over the past five years, although growth slowed to 28% from 2023–2025. FY2025 results are expected around 26 February, 2026.

In the most recent quarter, revenue accelerated to 41% YoY, reversing the slowdown.

ARP (average revenue per paid subscriber) increased 7% YoY, demonstrating pricing power and/or shift toward higher tiers (Duo Max).

Duolingo became profitable for the first time in 2023, marking a shift from investment mode to margin expansion.

Gross margin is a 72%, in-line with software apps rather than traditional education services.

Operating margin improved to 12.75%, up from 7.34% a YoY.

R&D spend remains high at 30% of revenue, but down from 50% at the time of IPO, indicating the company is scaling product without the need to scale R&D proportionally.

Stock based comp (SBC) totalled $308M over the past 12 months, roughly 4% of the market cap.

Balance Sheet

The company is debt-free and held $1.01B in cash as of the most recent quarter, though this includes 44% of deferred revenue from annual prepayments.

Fully diluted share count is expected to increase by 1% for the FY 2025, totalling around 4% of market cap for the past 4 quarters.

Cash Flow Statement

Free cash flow margin reached 28.5% as of the most recent quarter, up from 26.6% YoY.

Q3 2025 marks the first period the company paid income tax, driven by sustained profitability (tax expense: $239.49M).

6. Management & Governance

Duolingo is founder led and product driven. The company was built by computer scientists, not publishers or educators. That DNA and mission of the business continues to shape both culture and strategic priorities.

Luis von Ahn (Co-Founder & CEO, age 46)

Luis von Ahn is the driving force behind the company. A Guatemalan-born computer scientist, he sold his prior startup, reCAPTCHA, to Google in 2009 and was one of the early architects of human computation. He used distributed human behaviour to solve problems machines could not. He holds a PhD from Carnegie Mellon and has won numerous awards including a MacArthur Genius Fellowship (Genius Grant).

I’d recommend this How I Built This episode to gain an insight into von Ahn’s character.

With fast iterations, A/B testing at scale, behavioural experimentation and a reluctance to sell into institutions, Duolingo’s DNA can be traced back to von Ahn’s mission and guiding hand.

Von Ahn recently sold $17M worth of stock in multiple transactions across 2024/25. Despite this he still retains around 7.1% ownership in the company and receives only a conservative compensation of $767.25k (FY 2024).

Combined with CTO sales, total insider sales are worth monitoring but not necessarily red flags given IPO lockup schedules, low founder salaries and the fact that most compensation is equity.

Severin Hacker (Co-Founder & Chief Technology Officer)

Severin Hacker co-founded Duolingo while completing his PhD at Carnegie Mellon (and possibly has the best name for a CTO I have come across).

As CTO he oversees product engineering, machine learning and platform infrastructure. Hacker has not purchased shares on the open market and has sold stock regularly since IPO (approximately 90,000 shares across multiple transactions). Despite the sales, Hacker continues to hold a significant stake, with 2,886,917 shares, around 6.2% of the company.

CFO Transition - Matt Skaruppa Steps Down

Duolingo shares fell 7% after it was announced in January 2026, that CFO Matt Skaruppa would be stepping down. Skaruppa joined in 2020, helped guide the company through the IPO, oversaw the transition to profitability and built the internal finance function.

Investors will no doubt watch the replacement process closely.

Founder Ownership & Voting Control

Duolingo uses a dual-class share structure, allowing the founders to maintain voting control disproportionate to their ownership. This is similar to Silicon Valley software businesses including MET 0.00%↑ , AMZN 0.00%↑, GOOG 0.00%↑.

The dual-class structure makes hostile takeovers almost impossible and reduces activist pressure. It also means the founders can pursue long-duration strategies (AI tutors) without being forced to optimise quarterly profit.

Bear Case 🐻

1. Will Instant Translation Replace Learning?

Instantaneous translation services have long been available before AI was on the public conscience - think Google Translate.

However, AI is reducing the incentive to learn languages. Improvements in real-time translation, speech models and multimodal assistants raise the question, why invest years learning Spanish if AirPods, ChatGPT or Zoom can translate instantaneously?

The technology is no longer hypothetical, it has arrived. Zoom has already expanded its AI caption translation from 12 to more than 35 languages, and both Apple and Google appear to narrowing in on making real-time multilingual conversation seamless.

It’s worth highlighting that many users of Duolingo are not learning due to necessity - they are productively wasting time for fun. Google Translate has been available for a decade in the same period Duolingo’s growth has accelerated.

Serious learners, particularly those learning English, are doing so for economic opportunity, academic access or immigration and in most cases have to speak or understand the language fluently, without the help of AI.

2. Unforeseen AI Disruption

As LLMs improve further, there is the risk they become tutors and assessors, completely circumnavigating the need to platforms like Duolingo. Fears of this may be overblown by the fact that Duolingo is in a relatively niche segment and already out in front.

Duolingo is attempting to pre-empt this outcome by embracing AI. It was recently cited by OpenAI the Duolingo is a top token user, embedding generative models into tutoring and content production.

Management have stated that the cost of token usage is not directly affecting operational margins as only top tier, higher cost products (Duo Max) are incorporating the majority of workload, with users being charged accordingly.

3. Diversification Creating Product Drift

There’s a narrative that the expansion into music, math and chess detracts from the core language app (and main revenue driver). The additional segments allow the app to be viewed as a consumer learning platform. However, there’s an argument that these categories lack the same total addressable market (TAM) and monetisation potential of the language app.

According to the latest annual filing, neither has generated material revenue. Frequent Duolingo users are reportedly unaware that math, music or chess even exist within the app. The question is whether these additions improve the core app or distract from it. Math and Music launched in 2022 and 2023 respectively.

Language education supports adults who want to learn languages, ensuring the TAM is global and learnings are achievable on mobile. If Duolingo had initially launched with math or chess instead, it is difficult to imagine the app would have achieved 50 million DAU.

This does not mean diversification is a dead end. Music and language share cognitive and cultural importance, and AI tutoring could make these categories more economically attractive over time. For now, they represent novelty without monetisation and introduce the risk of strategic drift.

4. China, High Growth, High Fragility

China has quietly become Duolingo’s second-largest market by DAUs and one of its fastest-growing regions. Engagement and retention are strong, Max is now rolling out, and the long term monetisation potential around English is considerable. China accounts for only roughly five to six percent of revenue, but could act as a considerable revenue driver in the future.

The regulatory environment is unpredictable. The 2021 “Double Reduction” policy effectively banned for profit tutoring in core K–9 subjects, shut down IPO pipelines for ed-tech firms, and forced many companies to convert into non-profits. Duolingo sits outside that category, but history shows the Chinese state is willing to reshape markets overnight when education intersects with social policy.

Bull Case 🐂

1. AI Enablement

Rather than viewing AI as a threat to language learning, there’s an argument that AI enables Duolingo to implement new features that would previously have been impossible at scale.

The company has be quietly building towards and AI-enabled future for years. The adaptive learning engine, Birdbrain, launched in 2020. This feature adjusts difficulty in real time by estimating learner proficiency and exercise complexity - pushing learners without discouraging them.

Generative models extend Birdbrain’s reach beyond reading and writing into speaking, listening and conversation domains historically restricted to human tutors.

Duolingo’s long-term bet is that it can deliver a tutoring experience that is more engaging and as effective as a human instructor, with marginal costs approaching zero as the feature scales.

If successful, Duolingo could roll out this AI tutor to the serious-learner market.

Duolingo may be the only company on earth with the relevant educational dataset at this scale. This goes beyond right and wrong answers and includes error types, behaviour patterns, dwell time and dropout moments. If AI tutoring becomes commonplace, such data could provide a moat, not just the content.

AI may shrink the value of learning a second language, but it has yet to shrink the desire to learn one.

2. Founder-Led Execution and Culture

Duolingo remains founder led, and Luis von Ahn brings technical depth, prior entrepreneurial success and genuine product instincts.

Von Ahn owns just over 7% of the company, with co-founder and CTO Severin Hacker also retaining a meaningful stake and remaining operationally involved. The founders direct strategy and ensure it is still anchored to long-term value creation rather than quarterly optimisation.

That alignment is further reflected in compensation. Von Ahn does not take excessive remuneration by public-company standards, his base salary is modest (six figures), with the overwhelming majority of his wealth tied to equity value rather than remuneration. This ensures that his incentives are aligned with shareholders.

Historically, founder-led companies have tended to outperform over long time horizons, particularly in consumer software. The founders had prioritised engagement and learning outcomes for years before monetising, a trade-off many non-founder-led management teams struggle to achieve.

3. A Gateway into Consumer Education

With more than 50 million daily active users, Duolingo has a substantial consumer base from which to build.

Math, music and chess are early experiments in expanding the scope of learning. If the company can teach languages effectively, there’s the argument that it can transition to teach other subjects that will arguably also include AI tutorage.

This shift will likely take years, with management describing the app as “the best possible way to learn any major subject”. Regardless, the tens of millions of users offer an engaged foundation.

Once Duolingo becomes the default place where users go to learn on their phone, monetisation will not need to rely solely on subscription upgrades. Serious learners have far higher willingness to pay, especially in English-learning markets in Asia and Latin America.

Conclusion

A friend of mine made the comment that “If you had to delete a subscription, Duolingo would be the first to go.”

The business is a paradox. It’s almost incomprehensible that an app on which users spend two minutes a day on language exercises can generate the level of monetisation and financial performance that Duolingo has achieved.

There’s no doubt that Duolingo is an exceptional business, with free cash flow margins approaching 30%, return on equity near 40% and revenue growth still around 40%. And that’s alongside $1 billion in the bank (18% of market cap) without a penny of debt.

All of this has been accomplished within only a few years of turning profitable. This is not a normal ed-tech company, it’s a founder led growth engine.

The market remains sceptical, and not without reason. Duolingo is not a frictionless subscription business like Netflix, and it cannot convert the entire user base to paying customers without destroying the funnel that makes it valuable. The majority of the key users who need the app are subsided by wealthier ‘hobbyist’ customers.

The freemium model is a necessity. Shutting off the free layer would remove 90% of users and eliminate the primary source of future paid subscribers.

The app is not directly competing with Babbel or Rosetta Stone, it is competing with TikTok and Instagram for attention. Management has noted, churned users don’t ‘switch’ to rival apps, they stop learning altogether and go back to (mindlessly) scrolling.

Duolingo has turned gamification into something productive. Users may not emerge fluent after a few months, but they have made productive use of their time. The product teaches at approximately classroom-level proficiency, ingraining user habits.

The long-term strategic question is whether Duolingo has a moat? There is little intrinsic virality in the product, and the switching costs for casual learners are low.

However, the lack of virility also makes it harder for a well-funded competitors (think Google Translate) to launch a competing products overnight.

The more durable moat may come from data and ongoing education. The company arguably sits on the most extensive educational/learning dataset in the world, and it is now deploying AI to personalise content and close the gap between games and tutoring. If it succeeds in building a conversational, one-to-one tutor, it can move upmarket into the serious-learner segment, where annual revenue per user and and willingness to pay are far higher, especially for English learners in Asia and Latin America.

AI creates uncertainties at both ends of the spectrum. At the bottom end, real-time translation raises the question as to whether the wealthy consumer still needs to learn a language at all.

On the opposite end, AI makes Duolingo potentially more powerful, scalable and cost efficient than human tutors. The result may mean that AI may removes the wealthy tourist who wants a few phrases for the Amalfi Coast, but it empowers the Brazilian, Indonesian or Chinese students learning English for an improved quality of life. That latter cohort is both larger and more economically motivated.

The diversified expansion into math, music and chess suggests the company is testing whether it can become the consumer gateway to education.

The early experiments have not yet produced material revenue, and awareness remains low, but they do create opportunities outside of languages.

The next leg of growth will require building a product that serves a different audience with different needs. It’s unlikely this will be achieved through incremental tweaks to streaks and hearts, it will require reimagining the app and possibly business.

None of this should take away from the fact that Duolingo is generating more than enough cash to fund its own reinvention. It is willing to spend heavily on R&D, particularly AI, in pursuit of that the next stage of growth.

As a founder-led, technically competent organisation with tens of millions of installed users, it will provide the company with many opportunities to get the next stage right.

On the larger education picture, traditional institutions are likely more at risk from AI disruption than Duolingo, but going to university is as much about the comradery and rite of passage as it is about education.

Just because you can use AI to educate yourself about quantum-physics, doesn’t mean you will. Human connection, personal development and entertainment will still be core needs - and these are three areas that Duolingo will continue to tap into.

Whether Duolingo becomes a much larger education platform or only the most successful language-learning app will depend on its ability to cross that chasm. The bullish narrative has Duolingo as the future platform through which hundreds of millions of users learn not just languages but subjects more broadly. The bearish storey ends with a saturated casual market who are unwilling to subscribe.

At this stage, I’m unwilling to bet on the future of the passive-aggressive bird, but I’ll keep an owl’s eye on the rapidly falling share price.

Sources and Further Reading

https://www.acquired.fm/episodes/why-duolingo-worked-with-luis-von-ahn-ceo

https://investors.duolingo.com/investor-relations

https://blog.duolingo.com/growth-model-duolingo/

https://www.theverge.com/24267841/luis-von-ahn-duolingo-owl-language-learning-gamification-generative-ai-android-decoder

https://inpractise.com/articles/duolingo-risks-and-opportunities-of-llms

https://www.researchgate.net/publication/394827902_Evaluation_of_Duolingo_A_SWOT_Analysis/

https://assets.nextleap.app/submissions/DATAANALYSISOFDUALINGO-cfa09e78-96db-4653-9cc7-59f9659c88f4.pdf

Relevant Substack Articles -

Rob H. | Atomic Moat The Atomic Analysis: Duolingo (DUOL)

Christian Darnton Duolingo Is Netflix In 2022, Early Palantir Investor Explains The $1T Case.

Well written Sonny.

Glad to hear it from someone who used the app for a hot minute