Fractured Facebook?

Fractured Facebook?

The buying opportunity of the decade or a broken story.

Key Metrics

Market Cap = $359.84B

EV = 349.09

FCF = $35.8B

FCF Yield = 9.9%

ROIC = 24%

EBIT = $39.9B

EV/EBIT = 11.42

Intro

META 0.00%↑ share price is down two thirds since last year’s all time high. You would be down 20% if you invested 5 years ago. Investors have lost half a decade of compounding.

With the share price so badly beaten down, contrarian investors have started to question if now is the perfect buying opportunity?

Having reviewed Facebook/Meta in October last year, I thought it was apt time to take another look 1 year on:-

A broken story?

What has changed at Facebook in the past 12 months? Aswath Damodaran highlighted back in February that the share price was undervalued but had a broken story. Since then, things have only gotten worse. The business is facing ongoing macro headwinds, losses from the Apple privacy change, challenges from TikTok and pouring money into a supposedly wasteful metaverse bet. COO Sheryl Sandberg, largely credited with helping Zuckerberg build what exists today, stepped down in September. Things do not look rosy at Facebook HQ.

The social network may be facing the end of a prolonged growth period. Both revenue and users are stagnating. Q2 revenue was $28.8 billion, a decrease of 1% year-over-year.

What does the pricing suggest?

Meta is dirt cheap on a fundamental level. It’s the cheapest the stock has ever been. When you encounter technology companies trading at a PE of 10, you tend to think of also-rans like eBay and Intel. There’s no risk of bankruptcy, the company is still a money making machine, but the market is pricing it like its days are numbered.

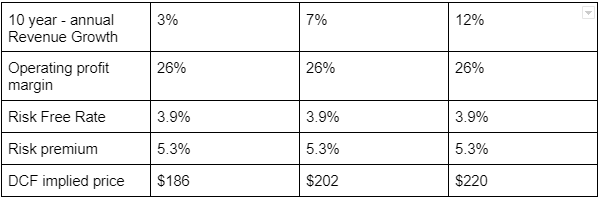

Using a conservative DCF, Meta currently offers a significant opportunity if Zuckerberg can turn things around. It’s impossible to predict how technology will change in 10 years (TikTok was still 4 years away from launching in 2012) making the DCF a finger in the air at best .

Assuming a conservative operating profit of 26% (2021 was 33%) and an annual capex/revenue ratio of 17% (2021 was 16%), Meta is undervalued in every scenario. By shoehorning in additional ads, revenue growth can track GDP and still be considered undervalued. Why is the stock so beaten down?

The Metaverse Play

Lets address the elephant in the room, investors and Mr. Market do not agree with Zuckerberg's Metaverse play.

Meta reportedly spent $10 billion on metaverse investments in 2021, approximately 50% of capital expenditures or 25% of net income. During May’s annual shareholder meeting, investors questioned whether the implementation of the metaverse platform to be ‘prudent or appropriate’.

To step out from Apple & Google’s walled gardens, Meta need their own direct-to-consumer software. The early signs are there, the Meta Quest 2 has reportedly sold 15 million units, outselling the Xbox Series X and S. Earlier this month, The New York Times wrote a surprisingly positive article on Meta’s Horizon software.

Whether investors are willing to wait whilst Meta bleed’s cash for 3-5 years, is another question. For the casual observer looking in, Meta appears to be making expensive bets which are burning cash, with little results.

It’s important to remember that Zuckerberg has more consumer data at his fingerprints than nearly anyone in history. The Metaverse bet is not a whim, it’s a calculated gamble and how Meta survives.

Customers were eventually going to stagnate due to population constraints. It’s not clear where the Metaverse wins will come from, the company doesn’t need to own (and likely never will) the entire Metaverse, but they are purchasing optionality on the next stage of computing.

Zuckerberg is betting big. The money machines, the family of apps, will continue to fund his metaverse expansion, until something works or he gives up.

Getting Revenue Back On Track

For any investor who has tracked Meta’s user numbers, it was obvious there were only so many addressable customers in the world. June’s earnings demonstrated daily active users across all apps of 2.88 billion, an increase of 4% year-over-year.

Single digit grow rates are not going to excite the market, but they are likely the reality for the foreseeable future. In the short term, Meta needs to recapture lost revenues of $10 billion from Apple's iOS change.

Earlier this month, Meta announced three new advertising types for Instagram, along with two new advertising types on Facebook, which are focused on the Reels format. New ‘profile feed’ ’ads mean that users may see ads while browsing through another person’s profile.

The new ad types indicate that Meta are increasing their ad-load, with the intention of maintaining short term revenue growth to keep investors happy

Reel It In

To challenge TikTok’s impending threat, the company is focusing on Instagram Reels. TikTok is now the app of choice amongst US teens; 63% use TikTok weekly, up from 50% last year, compared to 57% for Instagram, down from 61% the previous year.

Reels make up 20% of the time that people spend on Instagram. Over the quarter, Meta witnessed a 30% increase on engagement time with Reels across Facebook and Instagram. However, Reels doesn't yet monetize at the same rate as the main feed or stories, meaning in the near term, the faster that Reels grows, the more revenue they displace from higher monetizing sources. Reels ad revenue is only $1 billion annually, less than 1% of total revenue. At the risk of reducing revenue further, it’s apparent that Meta are adapting their apps to take on TikTok for the longer term, rather than appease investors in the short term.

Whilst TikTok’s growth has been nothing short of explosive, it’s not clear whether they can maintain it. YouTuber, Mr Beast, highlighted that he had only made $15,000 from TikTok, despite over a billion views. If creators drive views, TikTok will have to step up their own creator acquisition. Meta has been quick to point out that the new Reels ad updates will carry a 45/55 revenue-share agreement, with 55% of that revenue going to creators.

Global Growth?

Value Investigator made the compelling argument that revenue growth can come from South East Asia and India as GDP increases.

India’s GPD per capita was only $1,900.71 in 2020, compared to the $63,543.58 per capita in the US. With their billion person populations, these countries can bolster Meta’s revenues, but are decades away from making a significant difference.

Meta needs results now and it’s not entirely clear where that short term growth will come from. This is what terrifies investors.

Conclusion

The likely scenario in the next year or two is that Meta increases earnings by maintaining their aggressive buy-back policy. The company purchased a total of $44.5 billion in 2021, but scaled back its stock buybacks in the first quarter to an estimated $7.5 billion. $44 billion is 12% of today’s market cap.

Mr Market is treating Meta like the company is finished. Let’s be clear, in Q1 2022 the company still has 4 of the top 10 downloaded apps in the Apple & Google stores. The core advertising business is generating 50% operating margins on $120B of revenue. The company is very far from finished.

The board’s recent comments about Reels cannibalising other revenue suggest the hurt is not over for investors. In the short term, Meta is likely to double down new ad types and invest in Reels and AI targeting. This will challenge TikTok whilst clawing back some of the revenue lost to IOS changes.

Wins could come from unlikely places. In October, Meta launched AI software tools to ease switching between Nvidia and AMD chips. Meta’s investments in Reality Labs and the Metaverse should be viewed like Google's Other Bets, rather than a singular new platform. It is not an all or nothing win or loss. Some parts of Meta’s investment will pay off, others will be destined for failure.

The board recognises they can’t spend indefinitely and have highlighted, putting off some expenses to a longer timeline, whilst freezing hiring and cutting team sizes. Only 38, Zuckerberg could still be running the company three decades from now. The loss of Sheryl Sandberg is worrying, but the CEO has decades of experience and more to lose than anyone. His net worth has plummeted by $71 billion in 2022.

It’s easy to get caught up in the bearish scenario, however, Meta is a highly cash generative company with a FCF yield of almost 10%. It’s not clear when or where wins are going to come from, the only certainty is that long-term Meta investors are going to require patience and conviction. The buying opportunity of the decade or a broken story? Only time will tell.