PayPal Company Analysis - The World's Go-To Payment App

PayPal Company Analysis - The World's Go-To Payment App

A $PYPL deep dive

PYPL 0.00%↑ stats

Market Cap = $94.13B

EV = $95.38B

Gross Margin = 55.17%

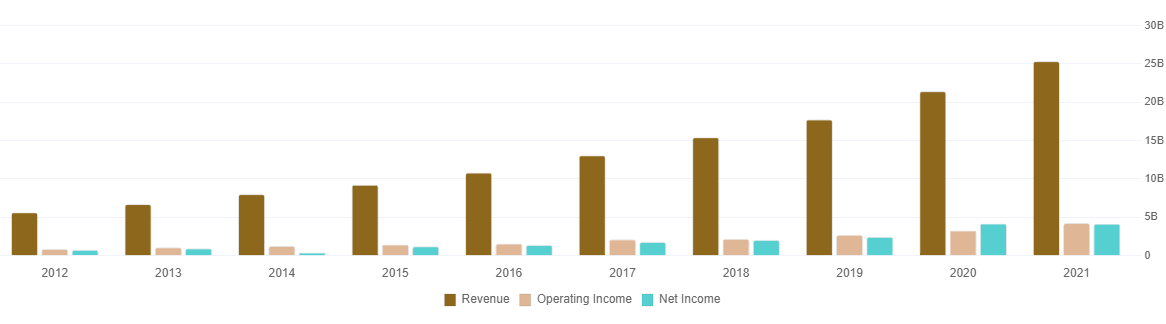

5 Year Rev CAGR = 14%

10 Year Rev CAGR =16%

FCF = $5.43B

FCF Yield = 5.4%

EBIT = $4.47B

EV/EBIT = 21.33

ROIC = 16%

Intro

PayPal’s ($PYPL) logo appears on almost every ecommerce checkout in the western world. The brand is recognised and trusted globally. The software allows customers to make and receive online payments.

Launched in 1998, its founders are now (in)famously referred to as the PayPal Mafia. The original company was established by Max Levchin, Peter Thiel and Luke Nosek in December 1998 and titled Confinity.

In March of the following year, Confinity was acquired by X.com, an online financial services company founded by Elon Musk. In October, Thiel replaced Musk as CEO of X.com, renaming the company PayPal.

PayPal went public in 2002 with a market cap of less than $1 billion. Within 6 months the company was acquired by eBay for $1.5B. At the time of the acquisition, every 1 in 4 transactions on eBay was facilitated through PayPal.

In 2015, PayPal was spun out of eBay, IPO’ing with a market cap of $52 billion. Dan Schulman, who previously held leadership positions at American Express, T-Mobile, and Virgin Mobile, joined the company as their new CEO. He remains in this position today.

Having lost 75% of their value since July 21’ highs, PayPal shares are now trading at their 2017 value, despite a 93% revenue increase and 132% increase in net income across the same time period.

The Business

As of 2022, PayPal is on track to achieve 430 million active consumer accounts, 29 million merchant accounts and a total payment volume (TPV - the total volume of transactions across the infrastructure) of $1.5 trillion.

PayPal deletes inactive accounts. This ensures all reported active user numbers are accurate. If the user does not log in for 180 days the company sends a notification to the customer before deleting their account.

PayPal is a classic example of a two-sided platform. The platform connects merchants and consumers. It gains valuable insights into customer behaviour through data, with the average user processing 45 transactions annually.

The core platform uses built-in tokenization to keep customer information secure. This ensures transactions are legitimate and identifies illegal, high-risk or fraudulent payments.

The company has built a portfolio of regulatory licences, enabling it to operate in markets around the world. This is a key competitive moat, without the licences it’s almost impossible to operate across numerous geographies. It would take considerable investment and financial resources by competitors to replicate.

Revenue Streams

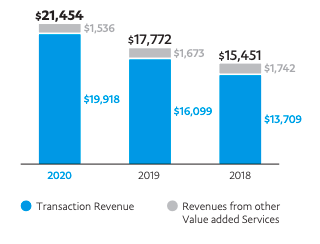

PayPal revenue is separated into Transaction Fees and Other Services.

PayPal makes 92% of revenue via transaction fees. The remaining 8% is generated by premium features offered to merchant accounts (in the form of subscriptions), the sale of card readers, business loans, referral fees on cashback rewards, interchange fees, interest on cash and promoting shipment services.

In 2021, transaction revenues grew by 17% to $23 billion. Like most online businesses, PayPal benefited from the shift from in store payments to online throughout the pandemic.

For customers, a monetary transaction is normally free. For merchants, the fee ranges between 1.90% to 4.99%, plus a fixed fee depending on the transaction type and amount.

Other Services

PayPal Here - PayPal Here is a point-of-sale system that allows merchants to accept in-store payments, whilst linking it to their online account.

Payflow - Payflow is a payment gateway that allows merchants to link their website to their processing network and merchant account. Merchants pay a fixed fee for every transaction ($0.10 in the United States). If merchants need more customisation capabilities, they can do so by opting into Payflow Pro, paying $25 per month.

PayPal Working Capital - Working Capital allows business owners to apply for loans issued by PayPal and repaid as a percentage of each transaction.

Pay in 3 - In September 2020, PayPal launched their buy-now-pay-later service. The offering enables users to pay for their purchases (ranging between $30 and $600) over a six-week period, in 3 instalments. Pay In 3 allows PayPal to compete with the likes of Affirm, AfterPay and Klarna, amongst others.

Interchange Fees - PayPal offers both a debit and credit card to consumers and businesses alike. Cards are provided in conjunction with Mastercard.

Acquisitions

PayPal has expanded its offerings by aggressively acquiring threats and competition.

Venmo (acquired in 2012), enables peer-to-peer payment applications, facilitating millions of transactions each year. Zettle enables merchants to be able to collect payments physically in person or by mobile payment.

PayPal’s other major acquisitions to date include -

July 2015: $890 million for money transfer company Xoom

February 2017: $233 million for bill payment management company TIO Networks

June 2018: $120 million and $400 million for Simility and Hyperwallet, respectively

November 2019: $4 billion for the browser extension Honey

Decoupling from eBay

PayPal has been eBay’s main payments provider since 2003. Originally announced in 2021, PayPal’s decoupling from eBay ends a two decade long corporate marriage.

CEO, Dan Schulman, highlighted that the eBay transition is expected to result in $600 million of revenue pressure for the first half of 2022.

Whilst eBay buyers can still pay with PayPal, sellers are now paid straight into their bank account, bypassing their PayPal account. eBay has replaced PayPal with Managed Payments, with eBay taking the transaction fee.

PayPal’s 10K states that ‘during the years 2021, 2020, and 2019, we earned approximately 6%, 13%, and 14% of revenue, respectively, from customers on eBay’s Marketplaces platform.’

Despite spinning out from eBay several years prior, there remains a clear driver of transaction revenue. 2021’s revenue of 6% demonstrates an obvious slowing on reliance, however, it appears that PayPal will encounter decoupling headwinds for the coming 24 months, until the separation is complete.

The Fintech Super App

There’s no doubt that PayPal views their future as an amalgamated super app. Throughout 2022 the company plans to roll out substantial changes to their mobile apps to integrate a range of new features.

PayPal’s acquisition of Honey, the shopping and rewards platform for $4 billion in 2019, appears to be driving this.

New features they are looking to add include enhanced direct deposit, check cashing, budgeting tools, bill payments, crypto support, subscription management, buy now pay later functionality plus all of Honey’s shopping tools.

These rollouts will transition PayPal from a payments app to a one-stop-shop finance app, creating a more competitive offering.

Customers will be able to deposit their salary, allowing funds to be used for daily life, including paying bills, saving or shopping. According to CEO Schulman, the rollout will be staged and tailored to the user.

As of June 2022, new features include buying/holding/selling crypto, paying over 3 payments, pay with QR codes and secure credit.

Bear Case

Aggressive competition and disruption - You cannot (yet) integrate PayPal into Apple Pay and the option is not straightforward on Google Pay.

Outside of China, there are approximately 1 billion mobile wallet users. PayPal should be leading them, but is lagging. Mobile wallets are bypassing PayPal completely, connecting the customers debit card and mobile.

Competitors continue to innovate in the online payments sector. Adyen and Stripe are gaining more traction in the payment processing space. Other competition includes Zelle, Shopify and Cash App. Competitors will seek to steal users by offering cheaper transaction fees, cannibalising margins and resulting in a race to the bottom. If PayPal cannot find a way to become the financial super app they covet, they will become a legacy product.

Headwinds - The eBay decoupling and return to normality post pandemic are producing some obvious headwinds. eBay’s transactions still accounted for 6% of Paypal’s revenue in 2021, down from 14% in 2019. The reliance on eBay’s customers is decreasing, but it’s not clear how much this will affect revenues before the decoupling is complete.

Bull Case

Globally recognised brand with consumer confidence - PayPal is one of, if not the, most trusted payments app in the world. According to Interbrand, PayPal was the 42nd most valuable global brand. With decades to build a loyal customer base, PayPal remains the western world’s go-to transaction app.

Infrastructure and regulations - PayPal has decades of software infrastructure and security as well as experience navigating global regulations. The global payments network is complex and not as straightforward as launching an app.

Strategic acquisitions - PayPal has been on an acquisition spree. They made several throughout the pandemic including, Paidy, Happy Returns, Chargehound and Curv. This follows 2019’s purchase of Honey. These deals are double pronged with the intention of reducing competition or increasing the core transaction volume. These acquisitions are driving the super app ambition.

Finally stepping out from eBay’s shadow - Despite causing headwinds and headaches, the decoupling from eBay will pass. This will allow the company to focus on strategic partnerships. Starting in 2022, customers will be able to use Venmo (PayPal subsidiary) to pay on Amazon. It’s unlikely synergies with other tech behemoths would have come to fruition had PayPal still been tied to eBay.

Conclusion

PayPal investors have had a volatile 24 months. From elated highs in summer 21, to depressing lows of May 2022. Despite this drawdown, PayPal has returned a 20% CAGR for shareholders since going public in 2015.

PayPal’s ambitions lie in owning the rails. Dan Schulman has laid out their plan. It’s not clear whether these transitions have had a material effect. PayPal doesn't just want to transition to a Super App, it needs to. Competition is coming thick and fast. Serious threats are attacking from all sides, Apple on mobile, Stripe and Square for transactions, Shopify at checkouts, the list goes on.

The company is at a crossroads. Regardless of aggressive competition, the user base and TPV continue to grow. They have made aggressive acquisitions to build upon their legacy offering. However, in such a disruptive market, they need to move fast to become Schulman’s coveted ‘super app’.

Despite a 70% share price pull back, it’s still not clear whether an EV/EBIT of 21.9 offers enough margin of safety to account for the encroaching threats.