Microsoft's Monopolies

A $MSFT company analysis

MSFT 0.00%↑ Key Metrics

Market Cap = $1.7T

EV = $1.65T

FCF = $63.3B

FCF Yield = 3.7%

ROIC = 26.1

EBIT = $86.7b

EV/EBIT = 19.03

Introduction

Microsoft is a company that needs no introduction. The business is synonymous with technology and software. Bill Gates has been one of the world’s richest men for the past three decades.

The company possesses a diverse business model, which includes Windows, Azure, Teams, LinkedIn, Xbox and GitHub, amongst others.

Founded in 1975 by Bill Gates and Paul Allen, the first version of Windows launched in 1995. Historically, Microsoft’s dominant business has been their operating system. In the late 2000’s it appeared that the business was stagnating. Investors punished the company, with a P/E as low as 11 in 2011. It took 6 years for the share price to recover after an almost 50% sell off.

The shift to SAAS and the launch of Azure supercharged the business. With a market cap of $1.7T, the company is third in size to only Apple and Saudi Armco.

The Turnaround

Less than a decade ago, Microsoft software was sold in boxes. The company faced similar challenges to other out-of-the-box software companies, such as Adobe. The move to a subscription model increased the addressable market, reduced the upfront cost and increased user numbers. Windows 10 marked the end of the packaged software, whilst the SaaS model created recurring revenue.

The catalyst for the turnaround was the promotion of Satya Nadella to CEO in February 2014. Nadella shifted the internal culture and created a collaborative approach, demonstrating a willingness to work with competitors. Under Nadella’s leadership the company made the bold move to write off the entire Nokia acquisition, viewing it as a lost cause, and halt Microsoft’s smartphone efforts. The CEO embraced the open-source software community, giving Microsoft credibility amongst developers.

The company has quietly carved out a niche in cloud services and SaaS, retaking its position at the top of the tech tree. Microsoft Azure is gaining on AWS and Office boasts 345 million paid seats.

Business Segments

Microsoft separates its business into three segments; Productivity and Business Processes, Intelligent Cloud and More Personal Computing. So how does the company make money?

Productivity and Business Processes

Microsoft's Productivity and Business Processes consists of Office (Commercial and Consumer), Teams, Outlook, LinkedIn plus other business solutions.

Office

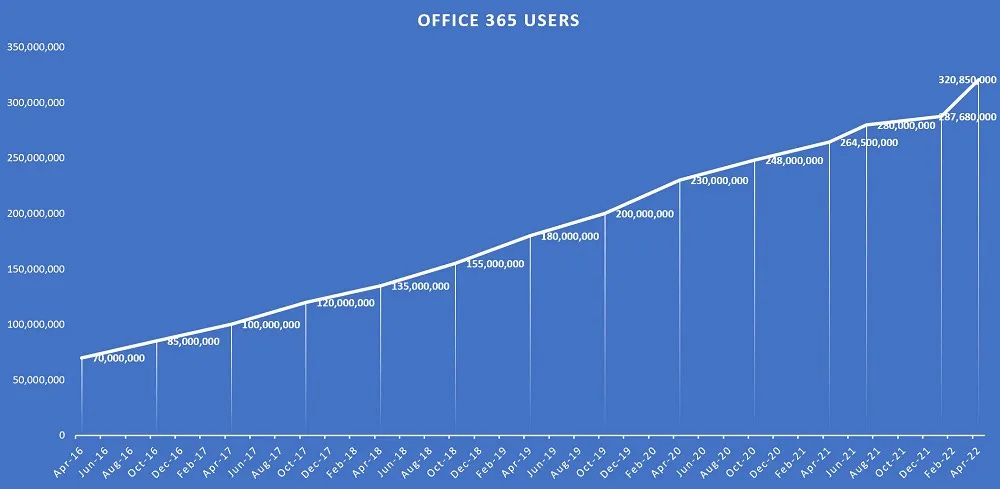

Office consists of notable apps including Word, Excel and PowerPoint. The software generated 13% revenue growth in 2021, not bad for a service that has been on the market for over three decades.

It’s difficult to pin down exact numbers but (pre pandemic) there were an estimated 1.2 billion Office users, with around 750 million regular Excel users.

Microsoft reports customers as ‘Paid Seats’. In April 2022, Office 365 reached 345 million paid seats. This equates to approximately 17% year-over-year increase in commercial revenue. It’s not clear how many companies these seats belong to, however, Statista have reported that there are over 1 million enterprise customers. These include HP, Ernst & Young and the NHS.

Teams

Teams, like Zoom and Google Meet, saw a significant uplift in user numbers during the pandemic.

Users automatically receive Teams when they purchase the Office Suite and Microsoft 365, giving the app an obvious advantage over competitors.

In January, Microsoft reported approximately 270 million monthly active users, up from 145 million in 2021. The company is no longer reporting daily active users, with the number slowing as a result of the return to the work place.

Microsoft acquired LinkedIn for $26.2B in 2016, with the aim of integrating it with their enterprise software. LinkedIn generated $10.3 billion revenue in 2021, an increase of 43% year-on-year, and almost 4x increase since Microsoft purchased the platform. LinkedIn now has over 822 million users.

LinkedIn makes Money from five different revenue streams -

Talent Solutions - connecting candidates and employers. In a July 2022 blog, LinkedIn revealed Talent Solutions surpassed $6 billion in revenue in the previous 12 months.

Marketing Solutions - generation of business leads. According to Statista, LinkedIn made $3.82 billion from advertising in 2021.

Sales Solutions - generates sales prospects.

Learning Solutions- online training and education.

Premium Subscriptions - additional access to users and solutions.

Intelligent Cloud

Microsoft’s Intelligent Cloud Segment consists of their cloud services, including Azure, and Enterprise Services. Microsoft only reports its 'Intelligent Cloud' revenue, which lumps Microsoft Azure in with Microsoft 365 and other productivity tools, making a direct comparison to AWS and GCP difficult. In 2021, Intelligent Cloud delivered $168 billion in revenue, up 18 percent year-over-year.

Azure

Azure is the driving force behind Microsoft’s turnaround. In the most recent earnings, the company reported a 35% rise in revenue for Azure, in comparison to 11% for the overall business.

In 2021, the cloud infrastructure market grew by 37% to £131 billion, according to Synergy Research data. Although AWS maintains its market dominance of 33%, Azure is gaining quickly. Microsoft highlights that AWS is up to 5 times more expensive than Azure for Windows Server and SQL Server.

Microsoft rents Azure capacity and services to customers, whilst using it as a backend for many of its own cloud-based products. Azure Active Directory has 550 million daily active users, an increase of 50 million in six months, and 125 million more since the 425 million milestone achieved in January 2021.

The fact that eBay is one of Azure’s largest customers demonstrates how Microsoft can benefit from Amazon competitors.

More Personal Computing

Microsoft’s More Personal Computing segment consists of Windows, Gaming and Search Advertising.

Windows

Microsoft generated $23.2B of revenue from Windows in 2021.

Microsoft has three types of licences for its products; Full Packaged Product (FPP) Licences, Original Equipment Manufacturer (OEM) Licences and Volume Licences.

Full Packaged Product (FPP) Licences - retail customers who require fewer than five licences.

Original Equipment Manufacturer (OEM) Licences - comes pre-installed on a new computer or device.

Volume Licences - These are predominantly purchased by enterprise customers including large businesses, organisations and educational institutions.

Xbox

Microsoft entered the world of console gaming in 2001 with the launch of the original Xbox. In 2021, the company generated $15.4B from their Gaming Segment.

The first three iterations of the consoles have sold over 160 million units. The fourth versions of Xbox, Series X and Series S, were released in November 2020.

In 2020, Microsoft purchased Doom and Skyrim publisher Bethesda Game Studios (via the $7.5 billion purchase of the parent company ZeniMax Media).

Microsoft announced the acquisition of Activision Blizzard in January 2022. They offered $68.7 billion in cash and are expected to complete the acquisition by mid 2023. The acquisition will give Microsoft a monopoly on several games including fan favourites, Call of Duty and World of War Craft.

In a world where the average gamer plays over 8 hours per week and each generation consumes more than their parents, Xbox provides a clear challenger to Zuckerberg's Metaverse aspirations.

Acquisitions

Microsoft is hedging their bets by making very shrewd acquisitions.

Microsoft has made fourteen acquisitions worth over one billion dollars;

Skype (2011)

aQuantive (2007)

Fast Search & Transfer (2008)

Navision (2002)

Visio Corporation (2000)

Yammer (2012)

Nokia's mobile and devices division (2013)

Mojang (2014),

LinkedIn (2016)

GitHub (2018)

Affirmed Networks (2020)

ZeniMax Media (2020)

Nuance Communications (2021)

Activision Blizzard (2022)

The $19 billion acquisition of Nuance, a software company that specialises in speech recognition and artificial intelligence, barely made headlines. Microsoft is making intelligent acquisitions that continue to fly under the regulators radar.

Bear Case

Besides the relatively high share price, it’s difficult to concoct a solid Bear Case that would see the company disrupted.

Too reliant on Azure - Azure is the driving force of the company. With a 35% growth rate in the most recent quarter, there are no obvious signs of a slow down. Azure faces competition from Amazon, Google, IBM, Oracle, but with the cloud services market only growing, Azure is quickly carving out a niche. Azure has largely driven growth for the past several quarters, however, if this was to slow, the effect would be a significant risk to the business and share price

Government regulation - Microsoft has barely set a foot wrong since Bill Gates was hauled in front of congress in the late 90s. They’ve quietly expanded several monopolies while making several significant acquisitions. In a world where Facebook have been forced to sell Giphy, a $400m acquisition, Microsoft are set to acquire a $60B Activision. It’s not difficult to understand who regulators favour. Governments appear to be cracking down on large organisations who publicly handle data, in particular Google and Facebook, whilst ignoring Microsoft. The oligopolies and large scale acquisitions could attract attention to the Big-Tech breakup advocates, but the company has avoided scrutiny…for now.

Activision Acquisition Goes Wrong - We have witnessed it before with the write off of Nokia. Microsoft is spending big to acquire Activision. For over a year, Activision Blizzard employees have protested against the company’s poor handling of ongoing sexual harassment allegations. Activision comes with issues and challenges. A lawsuit from New York City accused Activision Blizzard CEO, Bobby Kotick, of rushing to sell the company in a bid to escape liability.

Satya Nadella is a shrewd operator, but with 10,000 employees to integrate and ongoing lawsuits, it’s not going to be straight forward.

Bull Case

A global infrastructure the world relies upon - Whether it’s Azure, Office or Microsoft 365, the company's infrastructure is sticky and deeply integrated. Microsoft offers a full stack service which ties all their services together across the globe.

Great products are not the only key ingredient of Microsoft’s business model. With its long history, the company possesses many complex relationships with their enterprise customers.

Optionality on the next stage of computing - Whether this be from Xbox, cloud infrastructure or HoloLens, this company has several options on the next stage of computing. With technology driving towards either AI, the Metaverse or Web3, Microsoft is sure to profit.

Conclusion

Microsoft has achieved what few people thought possible a decade ago. The turnaround has been deftly navigated by Satya Nadella. The company demonstrates dominance in almost every market it participates. When the services are not dominant, they are part of an oligopoly. The business is investing across multiple fronts whilst making savy acquisitions.

Unless there is an unforeseen shift in computing (looking at you Zuck), it’s difficult to see a scenario in which Microsoft will be disrupted within the next decade.